Our investments and portfolio announcements

‘New’ alt assets are having their moment…

In just the last month, a digital artwork by Beeple sold for $69m, Jack Dorsey auctioned off his first ever tweet for $2.9m, and then, of course, this…

There’s no shortage of commentary on some of the technology and macro-drivers behind this, so I won’t labour on them here, but at a high level we’re seeing the perfect storm of:

- – A low interest rate environment creating a hunt for yield

- – Increasing consumer interest in investing in products and brands we know and love

- – Companies staying private longer, reducing opportunities in the public markets

- – Growing wealth flowing onto the blockchain

We have more investors, interested in more types of assets, and we’re finally getting the technological revolution required to enable this.

What really interests me, however, is not so much the ability to buy ownership of tweets, digital artwork or sports cards (although I’ve spent my fair share on Sorare recently), but rather the broader capital markets and wealth building opportunities for alternative asset classes as a whole.

Alt assets themselves are nothing new. Institutions and High-Net-Worth Individuals have been investing in ‘old’ alt assets, such as real estate, commodities and private equity for decades (and in increasing volume). But for consumers and SMEs, this is less the case. Many wealth-building assets have become increasingly inaccessible (e.g. property), remained stubbornly illiquid (e.g. start-up equity) or left unrecognised by lenders as collateral, therefore reducing opportunities for leverage.

It’s across these three areas of Access, Liquidity and Leverage, that I get most excited and where we’re actively investing at Mouro Capital.

OPPORTUNITY 1 – Improving Access

Compared to institutional investors, consumers (particularly younger ones) have historically suffered from a lack of access to some of the highest yielding alt assets. Real estate is a good example in this regard. The costs involved in buying a home and the divergence of property values from income growth have meant that many young people are finding it increasingly challenging to get onto the property ladder.

The same can be said for private equity and venture capital. An institutional favourite, venture capital as an asset class has largely remained inaccessible for everyday consumers. The minimum investment sizes have been too high and access to the top-performing funds has been out of reach.

But this need not be the case, and we’re starting to see some really innovative approaches to solving problems such as these.

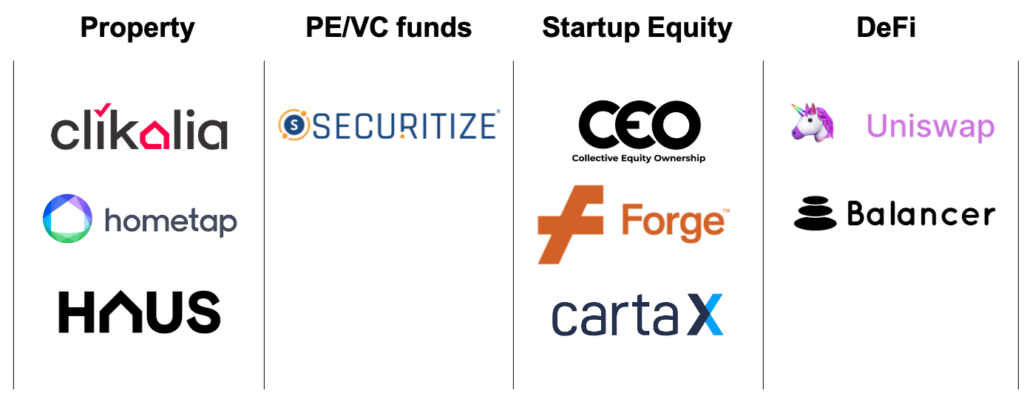

PrimaryBid, for instance, is opening up access to IPOs for everyday investors: Deliveroo recently used PrimaryBid to help their customers participate in their IPO and PensionBee has similar plans. Similarly, in property, ‘gradual ownership’ start-ups such as Divvy and Virgil are reducing the hurdle of getting onto the property ladder by co-investing alongside house buyers and allowing them to increase their ownership share over time. In a similar way to which DriveWealth (a Mouro portfolio company) enables the fractional purchase of US stocks and shares, these companies are breaking down larger assets and enabling fractional, incremental ownership of them.

But there’s still a long way to go…

Across the spectrum of alternative assets, we believe there are a number of market and infrastructure building blocks that need to be in place for access to truly flourish. These include:

- – High quality sourcing of the right assets

- – Fractional infrastructure to enable smaller investment sizes

- – Safe securing and storing of alt assets

- – A supportive regulatory regime

- – Tax efficiencies (where possible)

Our portfolio company CrossLend helps provide the complex data and regulatory infrastructure for the digitisation of private debt; we’re actively looking for start-ups that help solve such problems across other asset classes.

OPPORTUNITY 2 – Facilitating Liquidity

It’s widely held that investors should expect a higher yield on investments that cannot easily be converted into cash (known as ‘the liquidity premium’). And so, for investors with the right risk appetite, locking up cash in a longer-term asset can bring meaningful returns if managed as part of a diversified portfolio.

However, there are a number of asset types and cases where ‘rational diversification’ is not entirely possible, particularly where it involves assets that are more than just financial instruments and have an emotional connection.

Property is again a good example. For those fortunate enough to own a home, it often means the majority of their net wealth is locked into one asset, without diversification, and vulnerable to shifts in market price. Real estate is certainly not illiquid, but it involves a lot of time and cost when selling a home (as well as, of course, the emotional attachment). Homeowners can have vast wealth built up in a property, but only limited ways of unlocking it quickly and easily.

Similarly, for those who pursue an entrepreneurial venture, the equity a Founder or employee holds can appear extremely meaningful on paper but remains illiquid for many years until exit (if ever, given the high likelihood of failure). Entrepreneurs are often cash poor, having invested their savings early into the project, and are highly undiversified (‘all-in’ in the traditional sense of the phrase), with only limited opportunities to unlock any of that value if needed. Secondary transactions (whereby a Founder sells a portion of their shares during a financing round) are still fairly uncommon in Europe, and even less so for employees.

As illustrated by situations like these, it’s not uncommon for people to have a mismatch between their return-generating illiquid assets, and their shorter-term cash requirements for day-to-day needs. For assets where diversification isn’t a practical reality, liquidity has heightened urgency to mitigate the pitfalls of the ups and downs of life.

Fortunately, there are a number of startups attempting to tackle this. Mouro portfolio company Clikalia, for example, helps homeowners sell their home in only seven days, acting essentially as a market maker (or iBuyer in property terms). And for those who want to access their equity, but don’t want to sell their whole home, companies such as Hometap and Haus enable homeowners to sell fractional portions of their home to help finance shorter-term cash needs. Similarly, for start-up equity, there are companies such as Carta and Forge which help provide liquidity for shareholders.

I use property and start-up equity as examples, as they are both assets I have a strong personal connection with and investment in. But their challenges and solutions have commonalities with many other asset types. And in this regard, there is also a lot to learn and observe from DeFi. Over the past few years, DeFi has exploded, as has the ecosystem needed to support it. Uniswap and Balancer, for instance, are protocols for programmable, automated liquidity of crypto assets, playing a critical role in the efficiency of the space.

Whether it’s to provide liquidity for property, start-up equity, crypto or anything else, core foundations to help enable this include:

- – Cost efficient financialisation (be it via tokenisation, SPV etc.), to turn the asset into a financial instrument

- – Exchanges / marketplaces to enable the facilitation of trades

- – Market makers to help stimulate liquidity and price discovery

Again, we’re actively investing in this space, so please do get in touch if you’re tackling this.

OPPORTUNITY 3 – Enabling Leverage

For any type of wealth-building (be it consumer finance or company growth), leverage is a critical tool to amplify exposure and potentially increase investment returns (as well as, of course, risk). Put simply, leverage involves using borrowed funds to invest more than you currently have in cash. Well-known examples include taking out a mortgage to buy a home, or trading on margin with stocks and shares.

Key to unlocking leverage, however, is collateral, the security a lender has over a loan in case of default. Typically, the lowest cost and highest lines of credit are only available when they can be secured. Property is one of the most widely collateralised assets, but there are many other examples, including inventory, invoices, and even just cash. Regardless of the asset, the suitability as collateral is influenced by factors such as:

- – Ease of valuation (if you can’t value it, you can’t borrow against it!)

- – Price volatility, ideally stable and not too deflationary

- – Level of liquidity (it needs to be easily accessible if a default occurs)

With the rise of new alternative assets, we’re also seeing a corresponding increase in innovative forms of secured lending. Revenue-based financing companies such as Uncapped and a55 (both Mouro investments), for instance, are using future revenue as ‘quasi-security’ on a loan, with repayments made as a percentage of sales. And within DeFi, platforms such as BlockFi are issuing dollar-denominated loans using crypto as collateral. The list goes on, with future earnings (via ISAs) and employee equity just two other fascinating areas where the notion of collateral is being reimagined. Innovative lenders are starting to use new assets, data sources and valuation techniques to help secure their loans, which in turn is increasing opportunities for consumers and businesses to utilise leverage.

The possibilities are limitless. If an asset can be fractionalised, tokenised, valued, and has sufficient liquidity and stability, it could theoretically be used to secure a loan. What will we see next…? NFTs, almost certainly (e.g. NFTfi), VC carry (cough, hopefully), or maybe just knowledge itself (as already demonstrated to some extent in insurance with staking against smart contract risk via Nexus Mutual).

So that’s why I’m A-L-L in on alt assets. An inversion of the traditional phrase, but with no less conviction. If we can improve the Access, Liquidity and Leverage of alternative assets, consumers and SMEs can build wealth and navigate the ups and downs of cash flow, and life, in a way that hasn’t previously been possible. If you’re building products to help enable this, get in touch!

A version of this piece was originally published on Financial IT. Click here to access.

Click here to subscribe to our newsletter.