Our investments and portfolio announcements

Credit where credit’s due: the concept of buy now pay later (BNPL) in business-to-business (B2B) transactions has been around for centuries. Merchants have, for many years, agreed to let their trusted customers pay over time. Net terms of 30, 60 or even 90+ days have been, and remain, the most popular method of offline transaction. Now, as those marketplaces proliferate and more transactions move online, the question of how B2B terms will compete with card spending comes to the fore.

For many small and medium sized businesses (SMBs), waiting for outstanding receivables can be a matter of survival: posing a major source of cash flow issues. On average, companies wait more than 40 days to get paid which, in a lean environment, can make the difference between sink and swim. Time is money, even more so in times of high interest rates and economic uncertainty.

Traditional solutions like invoice factoring and discounting have been used to manage the issue by lending against receivables. The former, selling the unpaid invoice outright, while the latter loans a percentage of outstanding invoices, secured against the receivable ledger. In doing so, factoring companies get credit control over customers with outstanding invoices and suppliers don’t have to worry about chasing payment themselves (albeit with a dose of reputation management around collection practices to be considered in the mix).

Now, revenue-based finance can offer up a new alternative, giving SMBs access to working capital secured against future revenue to finance their inventory requirements. Take Mouro Capital’s portfolio company, Uncapped, for example. They offer growth capital of up to £10m to digital and ecommerce start-ups; generating flows of at least £10k per month that can be repaid as revenue is generated. In Latin America, a55 has a similar go-to-market strategy, targeting Brazilian and Mexican digital start-ups.

This does, of course, raise some considerations, not least trust. Merchant trust typically derives from a longstanding relationship that substantiates the supplier taking on credit risk on their own books. But these relationship-based models are not scalable, and companies that haven’t yet built a trusted credit relationship – most start-ups, due to the lack of long credit records or just because their activity is quite novel, thus misunderstood by incumbents – are driven to more traditional sources of finance via their banks, assuming they can even qualify for them. When the bank won’t offer acceptable credit terms or when a solution isn’t scalable to the merchant’s needs, a gap opens for new financing options. And this explains the increase in popularity of alternative credit sources like revenue finance and digital trade finance to bridge the void.

Innovating the space

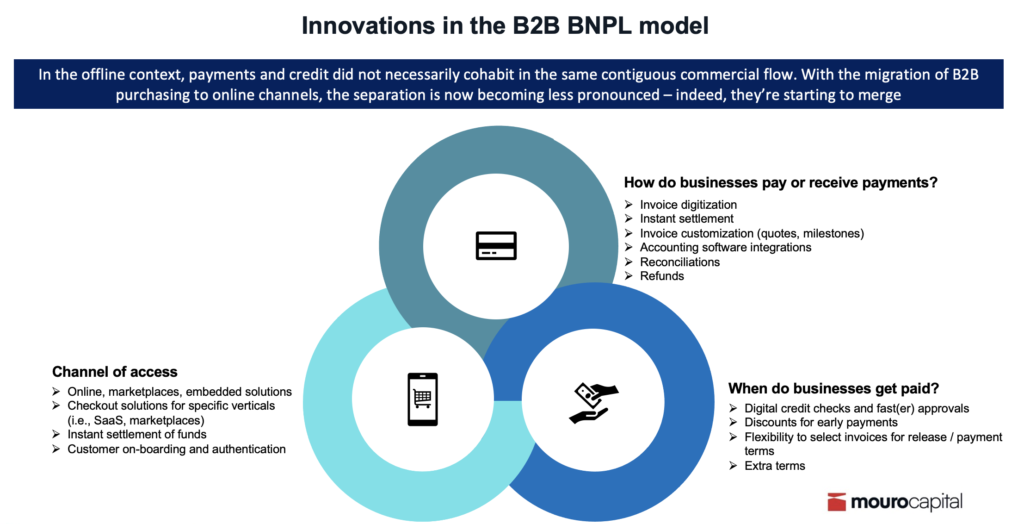

Three key questions mark the recent spate of innovation.

- 1. How do businesses pay or receive payments?

- 2. When do they get paid?

- 3. Where are services being accessed?

At the payment level, nearly all new developments have involved digitising invoices: giving companies the option to issue digital quotes or invoice by milestone or recurring payments, to digitally reconcile and issue refunds and to integrate at various level of the procurement flow, being it the purchase order or the inventory level.

From the credit perspective, merchants are being offered new options to manage credit risk, for example, by choosing a specific invoice to release, rather than release the whole portfolio, as happens in factoring. This provides merchants with more control and a more granular access to credit, which can optimise economics benefit relationships merchants have with certain commercial partners. Other innovations offer some flexibility around dunning and collections or incentivise early payment through discounts or other favourable terms.

B2B transactions can pose buyer-side challenges too, as most SMBs have limited access to working capital and more flexible payment terms can be an important support tool. Recently, corporate card issuers and expense management businesses have entered the space to offer procurement and spend management options. As they seek to become the hub for all things ‘financial management’, they too are developing their own credit solutions.

More generally though, we’re seeing new merchants shift away from traditional trade finance providers in response to the too-slow evolution of their offerings, perceived excess cost and ability to digitise or adapt to new digital channels. It’s a step change in who is accountable for selling these services. Take Mouro Capital portfolio company, Nowports, for example: they’re providing working capital solutions to finance inventory, and increasingly, suppliers are taking it upon themselves (either on their own or through partnerships) to offer terms as a route to online customer acquisition and B2B trade.

In the offline context, payment and credit dimensions were traditionally kept separate as both processes did not necessarily cohabit in the same location or in the same, contiguous commercial flow; but, with the migration of B2B purchasing to online channels, the separation is now becoming less pronounced – indeed, they’re starting to merge. New players are developing online payment and credit facilities embedded at checkout. Another of our portfolio partners, Kriya (fka Market Finance), offers a solution called PayLater that lets suppliers receive instant payment, while buyers can choose to pay it back on terms or in instalments, with up to 90 days interest free.

With a B2B market covering trillions of dollars in volume, the scope for growth among addressable merchants in Europe alone is significant. Existing marketplaces are relatively small, and change is tending to happen at the lower (smaller) end of the market because plug-in to enterprise resource planning tools can be tricky for larger, more complex legacy businesses. Most B2B BNPL providers work as an alternative to corporate and credit cards in targeting lower value transactions.

So, if B2B commerce is about to take off in a big way, what needs to happen to make it fly? Accepting payments is a basic enabler, since supplier models will need to find a more scalable, digital solution to their typical offline, relationship-driven model of assuming credit risk. In addition, infrastructure and business processes need to adapt to new and emerging channels to incentivise the shift from off- to online. This includes things like customer support and digital marketing to help increase adoption, enrich the customer experience, and increase volume through online channels.

As these things start to happen, and as payments and credit increasingly converge, a new digital lending model should start to emerge, under the banner of BNPL or embedded solutions. We believe successful businesses in the space will differentiate along the following lines.

• Cross-border capabilities. An increasing share of B2B transactions are performed across border but credit bureaux are local. We see the ability to underwrite seamless cross-border transactions as key for success.

• Underwriting capabilities. Given the higher price point of business purchases, B2B sellers tend to work with fewer buyers and are protective of the buying experience. As a result, any potential BNPL company needs to attract sufficiently high approval rates, while still applying prudent limits and collection processes. Naturally, there will be defaults, but the quality and sophistication of underwriting models will ultimately decide who has access to the best terms. Underwriting needs also to adapt to be able to score anywhere from a long-standing relationship to a one-off single transaction between unknown parties, to realise the full potential of the opportunity and the addressable market.

• Debt terms. B2B transactions are 10 times higher than direct to consumer tickets, which means business BNPL providers will need more debt, more equity, and potentially be less cash efficient than their B2C counterparts. To reach scale means deploying and rotating more or less large sums of capital at speed. Ideally, also, debt terms can be flexible and be adaptative to the sales cycle and state of inventory and sales of the participants at each point in time. Commerce requires utmost flexibility and adaptability, and so should the debt terms that support it.

• Quality of integration. Plugging-in to the processes of larger, potentially regulated entities is a highly complex procedure. At best, this can act as a moat, if not full-blown barrier to entry in some markets or sectors. As such, the quality of integrations will dictate how quickly a partner can be onboarded and start transacting smoothly. Integration is data, and data is the basis for all success factors herein.

• Segmentation:

- ◦ Larger small- to medium-size enterprises or corporates with turnover around 10 million or more have set processes in place and are driven by price and access to capital.

- ◦ At the higher end of the market, players have adopted technology automation such as xero and sage integrations, which allow products like overdrafts attached to debtor books and can replace traditional ID offerings.

- ◦ Players who offer a wide range of options, adaptable to their customers’ needs – revolving credit facilities/asset finance and so on – can expect to gain maximum benefit.

Taken together, this all means that the age-old promise of buy now pay later is entering the modern era. Undeniably, we’re still at the early stages of a more dramatic reinvention but, as traditional lines between payment and credit gradually evaporate and more and more B2B transactions migrate to online platforms, the ‘later’ part of this equation is starting to look increasingly interesting.

Click here to subscribe to our newsletter.